Green banks are starting to draw attention in the U.S., particularly since the federal government announced its first grant competitions under a national green bank program to bring clean technology and more affordable energy to low-income communities.

But installing more solar and wind electricity generation isn’t the only way green banks can help.

Massachusetts is launching an innovative new green bank that could become a model as states try to manage two crises at once: lack of affordable housing and climate change.

While most green banks focus on clean energy, the Massachusetts Community Climate Bank is specifically designed to boost the state’s stock of sustainable, affordable housing. It comes at an opportune time: States can now tap into billions of dollars in new federal funding for green banks under the Inflation Reduction Act.

So what exactly is a green bank, and how might it work for sustainable housing?

What is a green bank?

Despite the name, green banks aren’t traditional banks. They function more like investment funds with a mission to promote sustainability.

Green banks are public, quasi-public or nonprofit entities that use public funds to encourage private investment in low-carbon, climate-resilient infrastructure.

By using innovative financing strategies, green banks can lower the risks for private investors to support projects, which reduces the amount of public money needed to reach government goals like expanding renewable energy or, in this case, affordable housing.

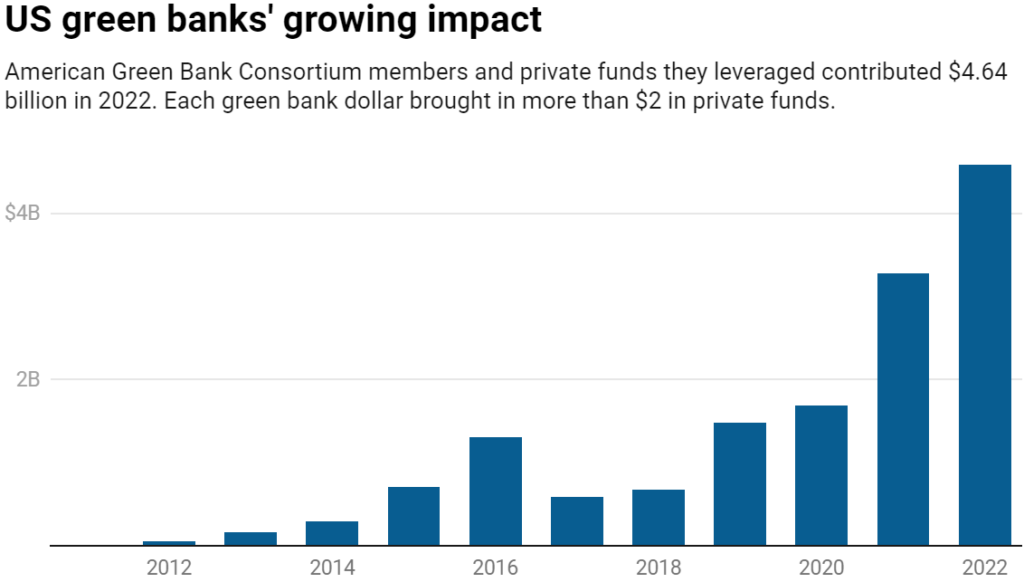

Green banks across the US

The U.S. had about two dozen green banks operating in early 2023 in at least 18 states and the District of Columbia – most of them focused on accelerating the transition from fossil fuel use to clean energy. And more were being developed.

In 2022, those banks used US$1.51 billion of public money to mobilize $3.12 billion in private investment. Since 2011, they have brought in a total of $14.8 billion.

Chart: The Conversation/CC-BY-ND Source: Coalition for Green CapitalGet the dataDownload image Created with Datawrapper

Each bank is slightly different. Connecticut’s was the first state-run green bank in the U.S. It started with a renewable energy focus but expanded to include sustainable infrastructure, climate resilience, water, waste and recycling projects. Michigan created a nonprofit green bank called Michigan Saves that provides financing for energy efficiency. Hawaii’s state-run green bank boosts solar energy use.

At the local level, Maryland’s Montgomery County has been financing rooftop and community solar, energy efficiency and electric vehicle charging infrastructure through a green bank since 2016.

Finance New Orleans is a particularly instructive comparison – the 40-year-old housing finance agency recently transitioned to a climate-oriented business model to finance energy efficiency, stormwater management and green infrastructure projects for homeowners, businesses and local governments.

A green bank for sustainable housing

The new Massachusetts Community Climate Bank is solely dedicated to climate-friendly and resilient affordable housing to meet the goals of the state’s Climate Plan for 2050.

That might include upgrading insulation and windows in older housing complexes to make them less leaky on hot and cold days, transitioning to electric household appliances such as heat pumps or adding solar panels and electric vehicle chargers.

Residential buildings are one of Massachusetts’ largest sources of greenhouse emissions, accounting for 19% of the total. Making housing more sustainable would cut those emissions and also help cut emissions in other sectors. For example, rooftop solar panels can reduce the demand for electricity from natural gas-fired power plants, allowing the state to close the plants or run them less often.

An affordable housing development in Chelsea, Mass., a Boston suburb that has been under pressure from rising housing prices. David L. Ryan/The Boston Globe via Getty Images

The challenge is that the finance industry tends to view new technology and low-income households as risks.

Green banks are able to use public money to “de-risk” such investments. For example, they can lend at low rates to private or local lenders on the condition that they lend money at affordable rates for customers to electrify their heating. Other financial instruments include loan guarantees, securitization and co-investment.

Massachusetts’ green bank started with an initial $50 million in state funds, but it expects to grow by attracting both private investors and federal funding.

The timing is strategic. The Inflation Reduction Act, passed by Congress in 2022, includes funding for green banks. Among other commitments, it creates a $27 billion Greenhouse Gas Reduction Fund, $20 billion of which is earmarked to be awarded to nonprofits to invest indirectly in green projects through other local financing entities – including green banks.

Lessons from green banks around the world

The Climate Policy Lab at Tufts University, where we work as researchers, studies green banks around the world.

We have found that by following a few foundational principles, green banks can increase financing for climate priorities while remaining financially viable and without creating housing debt that owners can’t pay back. These organizations should:

- Have a clear, well-defined mission.

- Be profit-making, but not profit-maximizing.

- Address market gaps rather than competing with private investment.

- Be flexible enough to use a variety of financial instruments.

- Have an independent, stable and nonpartisan governance structure to ensure stability.

The Massachusetts green bank has a sector-focused mission that targets a market gap. Its focus on affordable housing could be clarified even more by tying it to the state definition of disadvantaged communities. The New York Green Bank does this by aiming to have $100 million – about 35% of its total – invested in green housing to benefit disadvantaged communities by 2025.

A new sustainable apartment building in New York’s Rockaways neighborhood shows how solar panels and geothermal energy can help offset electric, heating and cooling costs for low-income residents. AP Photo/Mark Lennihan

Focusing the Massachusetts bank’s climate mission will involve some tough decisions. For example, Connecticut’s Green Bank supports gas appliances above defined energy efficiency thresholds, but there is an argument for leapfrogging gas entirely to support the electrification of heating and cooking instead.

What else should green banks prioritize?

Reducing greenhouse gas emissions is important for curbing future climate change, but communities will also have to adapt to the climate impacts ahead.

The fact that the Massachusetts green bank is dedicated to affordable housing is already one adaptation. People who have homes are far more protected from climate impacts than those who do not. And if those homes are powered by clean energy with lower utility bills, low-income residents can more easily afford to cool their homes in extreme heat waves.

Green banks could also fund climate resilience, such as adding green spaces around buildings for natural cooling. Research shows that affordable housing in the United States is often in highly vulnerable locations, such as those at risk of flooding.

The Connecticut Green Bank, for example, is piloting “Property Assessed Resilience,” which allows homeowners to borrow for flood protection upgrades and benefit immediately from increased property valuations and reduced insurance premiums. They can repay over decades through modest increases in their property tax bills.

Focusing on the scarcity of affordable housing can reduce both emissions and socioeconomic inequity simultaneously. In our view, that is the holy grail of climate policy.

Related Posts

Nonprofit hospitals have an obligation to help their communities, but the people who live nearby may see little benefit

Nonprofit hospitals have an obligation to help their communities, but the people who live nearby may see little benefit What nonprofit boards need to do to protect the public interest

What nonprofit boards need to do to protect the public interest Nonprofits serving or led by people of color get less funding than similar groups led by white executive directors

Nonprofits serving or led by people of color get less funding than similar groups led by white executive directors Why power skills – formerly known as ‘soft skills’ – are the key to business success

Why power skills – formerly known as ‘soft skills’ – are the key to business success How the end of carbon capture could spark a new industrial revolution

How the end of carbon capture could spark a new industrial revolution