Christopher Decker, Professor of Economics, University of Nebraska Omaha

Don’t be overly fooled by seemingly rosy jobs data heading into the Labor Day weekend.

Yes, the U.S. economy added 187,000 jobs in August 2023 – faster than the revised 157,000 increase for July and above most analysts’ expectations for the month. And yes, gains were seen across most industries, with health care and social assistance adding 97,300 positions, leisure and hospitality boosting numbers by 40,000, construction up by 22,000 jobs, and 16,000 additional general manufacturing jobs.

But there was also enough in the data released by Bureau of Labor Statistics on Sept. 1 to give comfort – of sorts – to the “Jeremiahs” among us economists. I’ll explain.

While jobs were up, so too was the unemployment rate, which ticked up a modest 0.3% from July to 3.8%. And average hourly earnings increased by just 0.2% in the month to US$33.82 – working out to a rather paltry 8 cent increase.

To me, rather than indicating that the job market is moving along at a healthy clip, as some suggest, it shows signs of something else: a continuing slowdown.

Look at the long-term trend

The fact that, overall, jobs expanded a bit faster than expected doesn’t suggest that the economy is ramping up and inflation is going to spike again soon. Rather, it mostly speaks to the difficulty in predicting month-to-month movements. There’s good reason, perhaps, that economics is sometimes called “the dismal science” – we aren’t always that good at saying with certainty what will happen over the short term.

Monthly data has its place in making assessments and guiding policy, for sure. But focusing on just one month can be misleading as the data can be quite volatile.

The underlying trends are what matter more. And that is where I see signs of a slowdown.

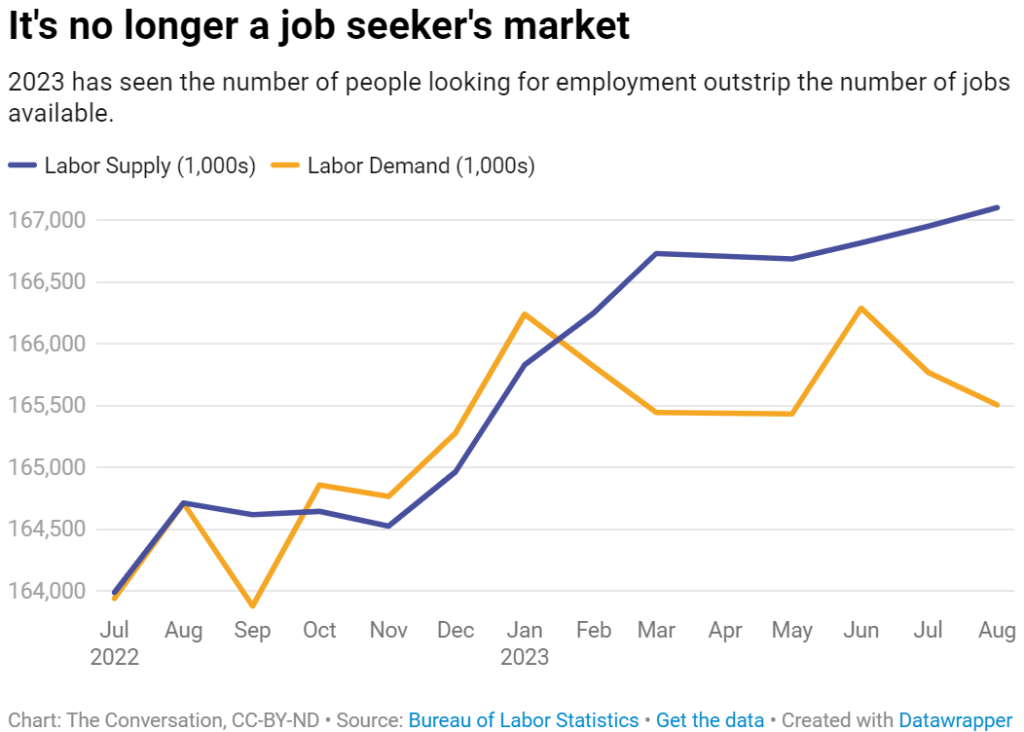

In 2022, labor demand – as measured by job openings plus nonfarm employment – exceeded labor supply, as measured by the labor force. In other words, there were more job openings than people willing to fill the positions.

As a result, we saw labor earnings increase by 5.1% relative to 2021. Great news for employees, but less so for the Federal Reserve: Higher wages combined with supply chain disruptions and the effect of war in Ukraine meant that the inflation rate, as measured by consumer price index growth, rose 7.7% in 2022.

To tame inflation, the Fed embarked on a program of aggressive interest-rate hikes. This resulted in a general economic slowdown by the beginning of 2023. The housing market cooled. Construction and related markets slowed.

But now labor supply is outpacing labor demand – there are more people looking for jobs than there are openings.

Based on the first seven months of data in 2023, wage growth has slowed to 3.4% compared to 2022, as has general inflation, slowing to 3.5%.

So where is the economy heading? The preponderance of the data is pointing to a general economic slowdown. As a result, some suggest the U.S. economy may be heading for a “soft landing,” where inflation rates reach 2% to 2.5% as the U.S. avoids recession.

But when it comes to the chances of recession, the economy is not quite out of the woods yet. True, inflation is trending down. But earnings have generally grown slower than inflation, resulting in a loss of purchasing power for consumers.

Less cash to spend on goods doesn’t appear to have hit the economy yet. Consumer spending in the first seven months of 2023 was up 1.9% on the previous year, by my calculations. However, there is evidence that a lot of this was due to consumers purchasing on credit. Credit card debt reached a staggering $1.3 trillion in the second quarter of 2023.

This is not sustainable. At some point soon, consumer spending will have to slow. And given that consumer spending represents about two-thirds of total GDP, a recession could still occur.

My best guess at the moment is that a recession is most likely to occur in early 2024, after the usual spending spree that is the holidays. But fortunately, thanks to the Fed’s recent efforts to decelerate the economy gradually, a major contraction is unlikely.

Related Posts

Companies haven’t stopped hiring, but they’re more cautious, according to the 2025 College Hiring Outlook Report

Companies haven’t stopped hiring, but they’re more cautious, according to the 2025 College Hiring Outlook Report Companies haven’t stopped hiring, but they’re more cautious, according to the 2025 College Hiring Outlook Report

Companies haven’t stopped hiring, but they’re more cautious, according to the 2025 College Hiring Outlook Report Goodwill created a new high school for dropouts − it led to better jobs and higher wages

Goodwill created a new high school for dropouts − it led to better jobs and higher wages Why people with autism struggle to get hired − and how businesses can help by changing how they look at job interviews

Why people with autism struggle to get hired − and how businesses can help by changing how they look at job interviews From business exports to veteran care − here’s what some of the 35,000 federal workers in the Philadelphia region do

From business exports to veteran care − here’s what some of the 35,000 federal workers in the Philadelphia region do